[quote]LankyMofo wrote:

PRCalDude wrote:

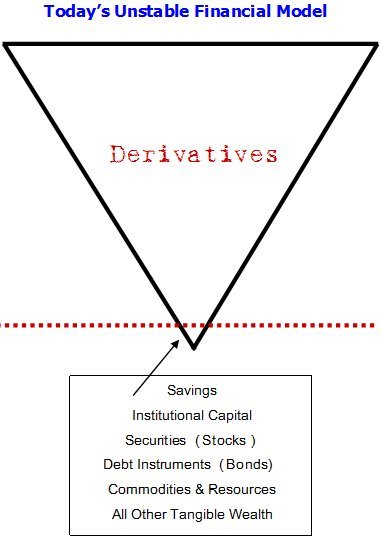

As far as which is bigger, reserves or losses, I think it’s anyones guess at this point.

The total amount of bad loans written was in the neighborhood of 4 trillion.

I believe you read more about this than I do but isn’t that still speculation? The banks haven’t written that much off, at least not yet.

Also, probably 80% (don’t ask where I got this number, I basically pulled it out of my ass by considering the decrease in the value of the assets) of that is recoverable through the auction of whatever assets the banks have to secure the loans (houses, mainly). The net 20% loss on $4 trillion (if that turns out to be correct) would be around $800 billion, or basically the same amount as the reserves.

The next couple years will be interesting.[/quote]

Failed Bank List from FDIC:

“Irwin Union Bank, F.S.B. Louisville KY 57068 September 18, 2009 September 22, 2009

Irwin Union Bank and Trust Company Columbus IN 10100 September 18, 2009 September 22, 2009

Venture Bank Lacey WA 22868 September 11, 2009 September 15, 2009

Brickwell Community Bank Woodbury MN 57736 September 11, 2009 September 15, 2009

Corus Bank, N.A. Chicago IL 13693 September 11, 2009 September 15, 2009

First State Bank Flagstaff AZ 34875 September 4, 2009 September 14, 2009

Platinum Community Bank Rolling Meadows IL 35030 September 4, 2009 September 14, 2009

Vantus Bank Sioux City IA 27732 September 4, 2009 September 14, 2009

InBank Oak Forest IL 20203 September 4, 2009 September 14, 2009

First Bank of Kansas City Kansas City MO 25231 September 4, 2009 September 14, 2009

Affinity Bank Ventura CA 27197 August 28, 2009 September 11, 2009

Mainstreet Bank Forest Lake MN 1909 August 28, 2009 September 11, 2009

Bradford Bank Baltimore MD 28312 August 28, 2009 September 11, 2009

Guaranty Bank Austin TX 32618 August 21, 2009 September 4, 2009

CapitalSouth Bank Birmingham AL 22130 August 21, 2009 September 11, 2009

First Coweta Bank Newnan GA 57702 August 21, 2009 September 11, 2009

ebank Atlanta GA 34682 August 21, 2009 August 25, 2009

Community Bank of Nevada Las Vegas NV 34043 August 14, 2009 September 18, 2009

Community Bank of Arizona Phoenix AZ 57645 August 14, 2009 August 19, 2009

Union Bank, National Association Gilbert AZ 34485 August 14, 2009 August 19, 2009…”

This list continues and is huge.

http://www.fdic.gov/bank/individual/failed/banklist.html

The great collapse is upon us. Hope everyone here has their survival farm all set up, in isolated environs.